Open30 Research Report

This report summarizes the research problem, methodology, walk-forward validation design, tracked results, limitations, and next experiments for the Open30 strategy research stack.

Summary

Open30 studies whether opening-session price action, prior daily context,

market alignment, and news sentiment can identify a favorable 30-minute trade

candidate after the market open. The current research stack builds candidate

rows keyed by (date, ticker, side), labels take-profit, stop-loss, and time

exit outcomes, then evaluates model decisions with rolling walk-forward

training.

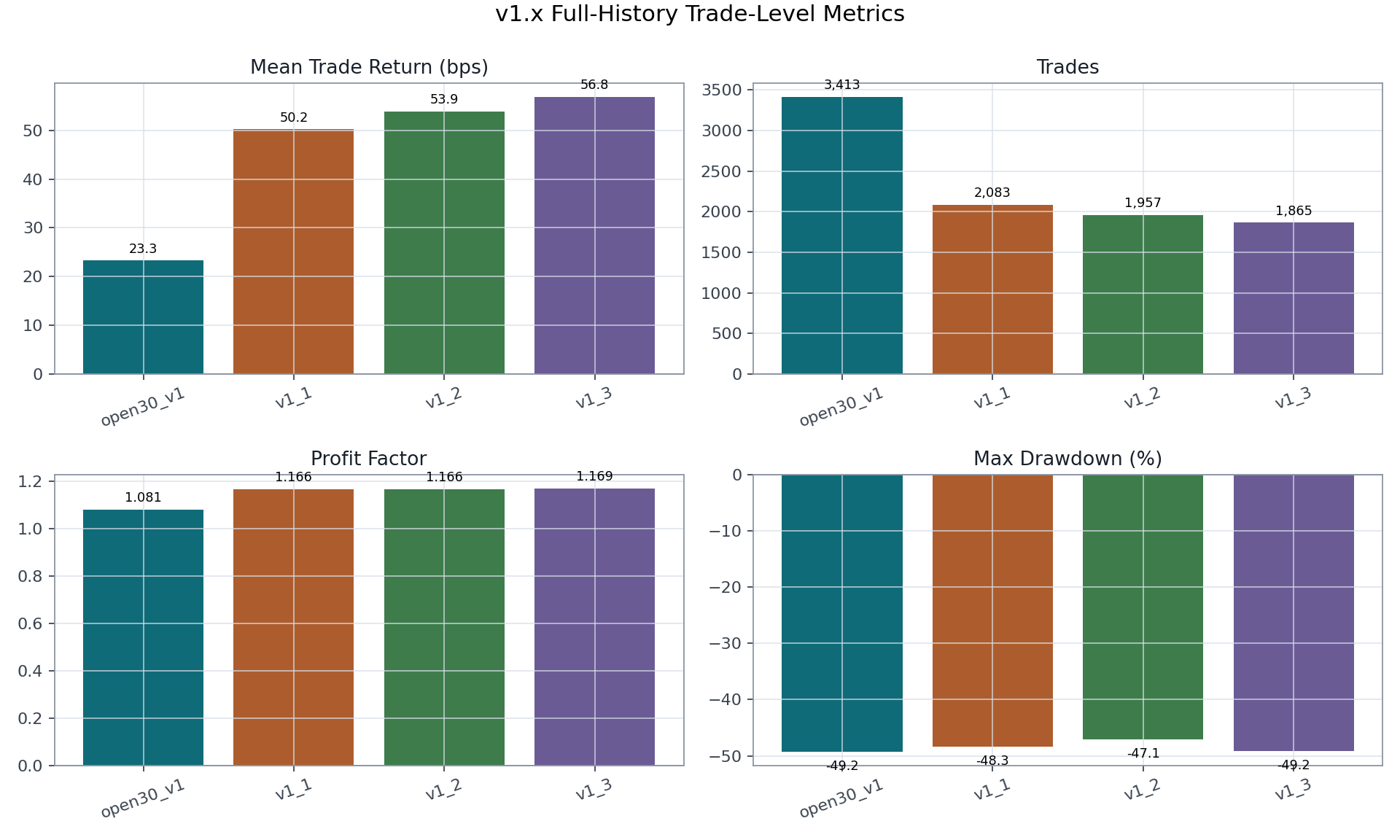

The strongest tracked full-history single-head branch is v1_3. It traded

1,865 days, averaged 56.82 bps per selected trade, and had a 1.169 profit

factor in the tracked artifact. The improvement audit finds that this edge is

execution-sensitive and should be hardened with realized cost modeling,

delayed-fill tests, point-in-time universe construction, and stronger

calibration.

Problem Statement

The strategy asks this: shortly after the open, is there one liquid large-cap equity candidate with enough expected return to justify a short-horizon trade through the first 30 minutes?

The research version evaluates candidates using historical minute bars, daily features, market context, and sentiment features. It does not claim a deployable trading system by itself.

Data And Universe

The pipeline expects:

- 1-minute bars at

data/raw/candles_1m.parquet. - Daily news files under

data/raw/news_daily/. - A tracked top-25 universe file at

data/interim/canonical/universe_top25.json. - Generated features, instances, labels, and final dataset under

data/processed/.

The tracked result metadata records 195,166 dataset rows and 3,983 trading days

for the main full-history runs. The public pipeline config starts ingestion on

2010-02-02; feature warm-up means the main tracked backtest rows begin on

2011-10-06. The fixed present-day top-25 universe is a known risk because it

can overstate historical performance through survivorship and concentration

effects.

The assembled dataset_open30m.parquet artifact is also available on Hugging

Face for readers who want to inspect or reuse the feature table without

rerunning ingestion and feature generation:

mospira/open30-equity-features.

Strategy Definition

The core strategy invariants are:

- Candidate rows are built per

(date, ticker, side). - Entry is the

09:31open. - Take-profit and stop-loss scanning runs from

09:31through09:59. - The time-exit proxy is the

09:59close. - Class mapping is

0=SL,1=TP,2=TIME. - Ambiguous rows are converted to worst case before simulation and scoring.

- Current canonical execution is long-only at decision time.

- At most one trade is selected per day in the canonical backtest.

The architecture manifests in architectures/ control reward multiples,

selection mode, training window, retrain cadence, embargo, calibration, stop

distance, EV thresholds, and position sizing.

Methodology

The pipeline builds features in stages:

- Fetch minute bars and news sentiment.

- Canonicalize sentiment to daily ticker-level records.

- Build daily, open-window, market-context, and sentiment features.

- Assemble feature rows keyed by

(date, ticker). - Build candidate trade instances keyed by

(date, ticker, side). - Generate labels for reward multiples.

- Assemble

data/processed/dataset_open30m.parquet.

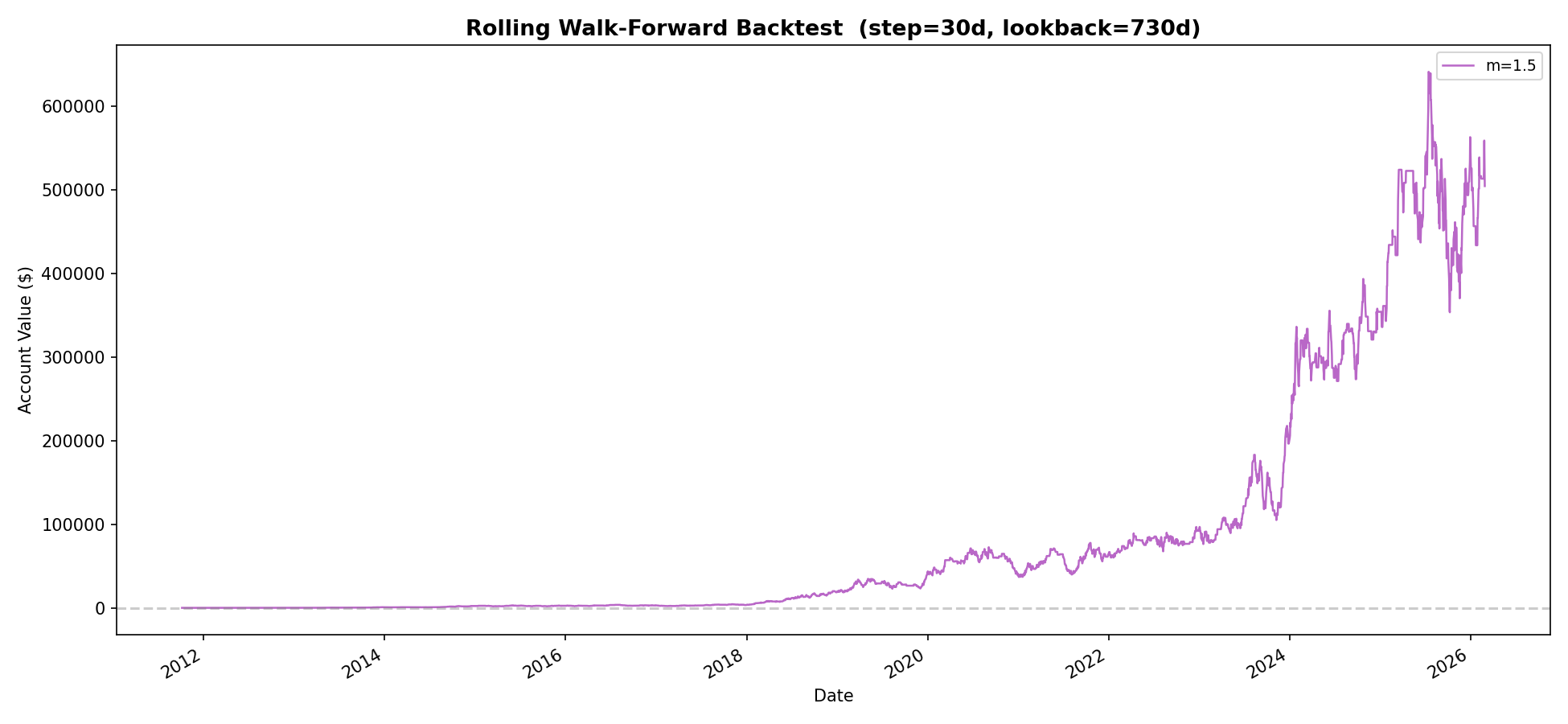

The backtest uses rolling walk-forward retraining with a 730-day lookback, 30-day retrain step, and 1-day embargo in the tracked full-history artifacts. Training currently uses long-side rows unless an experiment deliberately changes that policy. Probability calibration uses isotonic regression.

Architecture Versions

| Architecture | Purpose |

|---|---|

open30_v1 |

Raw-EV baseline centered on m=1.5. |

v1_1 |

Single-head m=1.5 with dynamic EV threshold tuning. |

v1_2 |

Tightens the dynamic threshold grid by removing low values. |

v1_3 |

Raises the minimum dynamic threshold to 0.075. |

open30_v2 |

Multi-head XGBoost setup with an expected-return meta selector. |

Results

Single-Head v1.x Branch

Account curves are sensitive to starting capital and margin policy. The table

therefore emphasizes trade-level metrics. open30_v1 also used a different

starting capital from v1_1 through v1_3, so account return should not be

read as a clean architecture comparison.

| Architecture | Trades | Mean trade return | Profit factor | Max drawdown |

|---|---|---|---|---|

open30_v1 |

3,413 | 23.28 bps | 1.081 | -49.24% |

v1_1 |

2,083 | 50.22 bps | 1.166 | -48.31% |

v1_2 |

1,957 | 53.90 bps | 1.166 | -47.11% |

v1_3 |

1,865 | 56.82 bps | 1.169 | -49.16% |

The metric comparison highlights the central v1.x tradeoff: the threshold variants select fewer trades, but the selected-trade return and profit factor improve relative to the raw baseline.

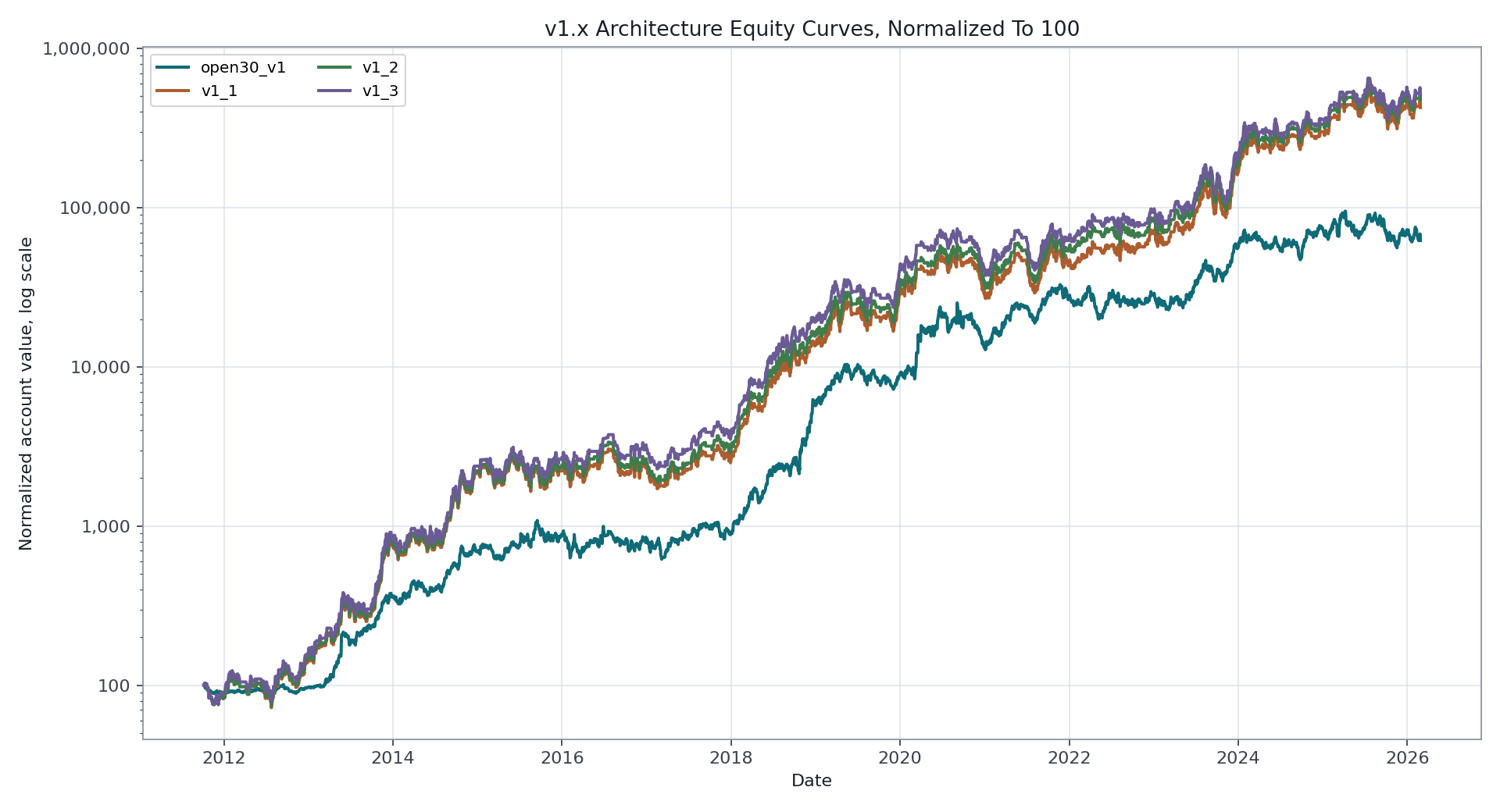

The normalized equity chart puts the v1.x variants on the same starting value. It uses a log scale because account values compound across a wide range.

The threshold variants reduced trade count while improving mean selected-trade return. Drawdowns remain large, so this is not yet a robust production claim.

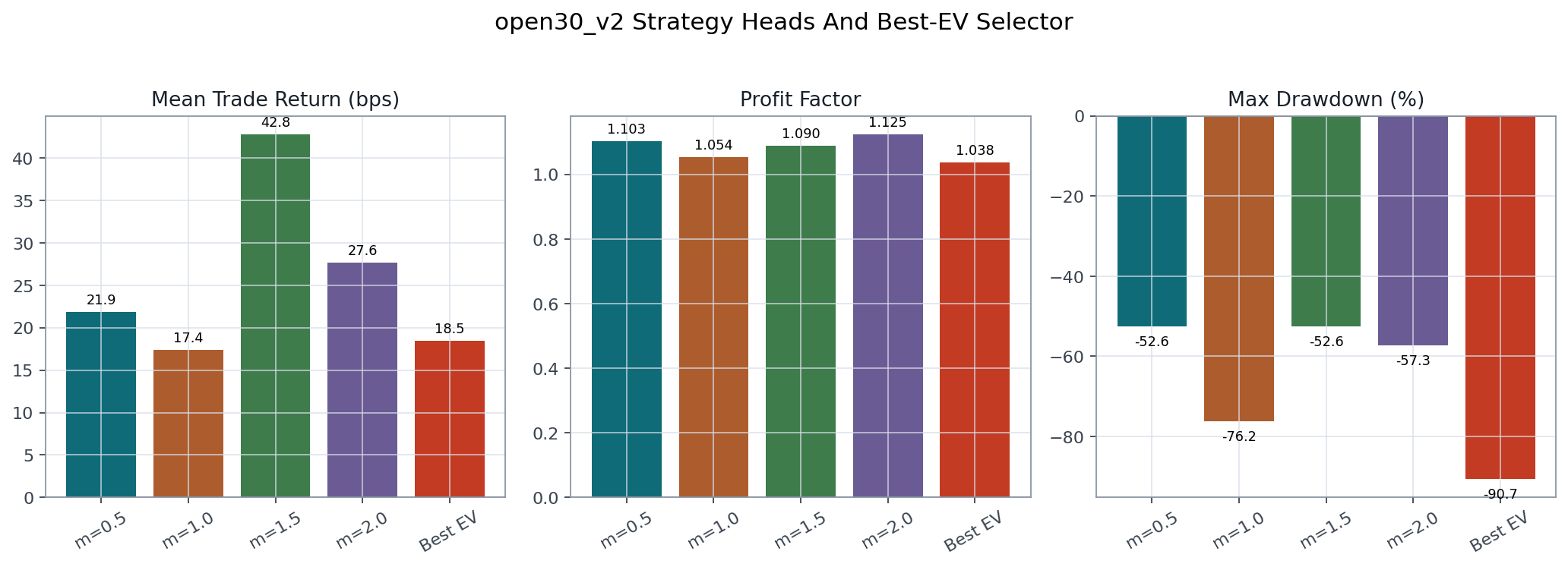

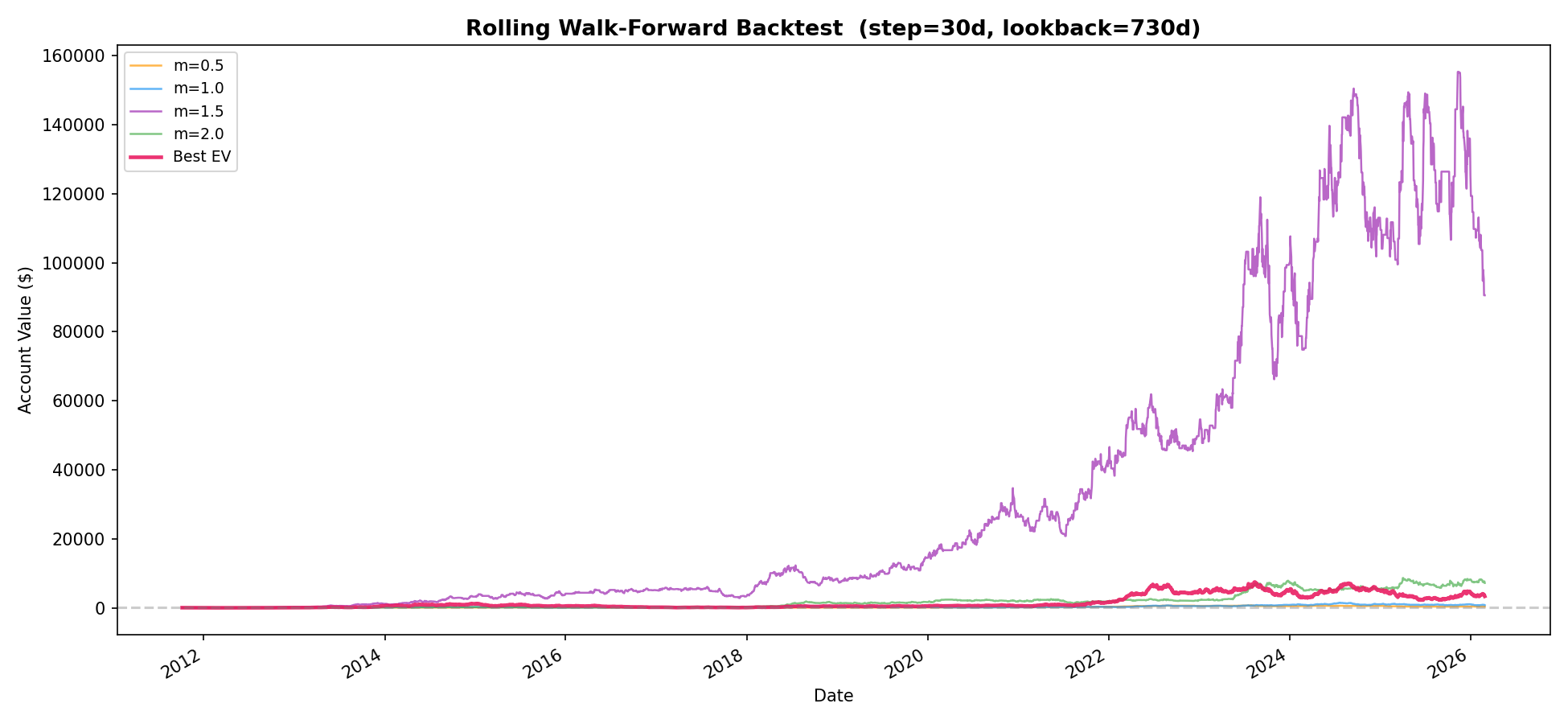

Multi-Head v2

The multi-head expected-return selector did not beat the stronger single-head branch in the tracked artifacts.

| Strategy | Trades | Mean trade return | Profit factor | Max drawdown |

|---|---|---|---|---|

m=0.5 |

873 | 21.89 bps | 1.103 | -52.60% |

m=1.0 |

2,089 | 17.40 bps | 1.054 | -76.25% |

m=1.5 |

1,972 | 42.83 bps | 1.090 | -52.60% |

m=2.0 |

2,080 | 27.65 bps | 1.125 | -57.29% |

Best EV |

3,254 | 18.50 bps | 1.038 | -90.66% |

The m=1.5 head had the best mean trade return in this v2 run, while the

Best EV selector increased trade count but had the weakest drawdown profile.

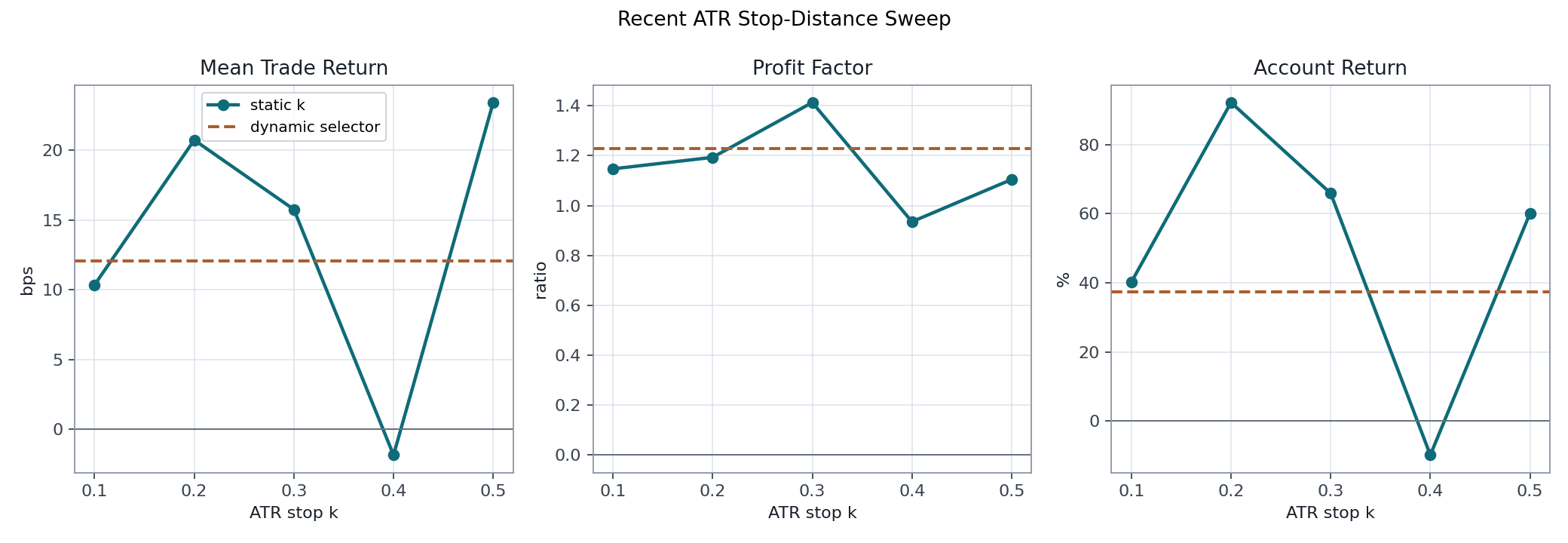

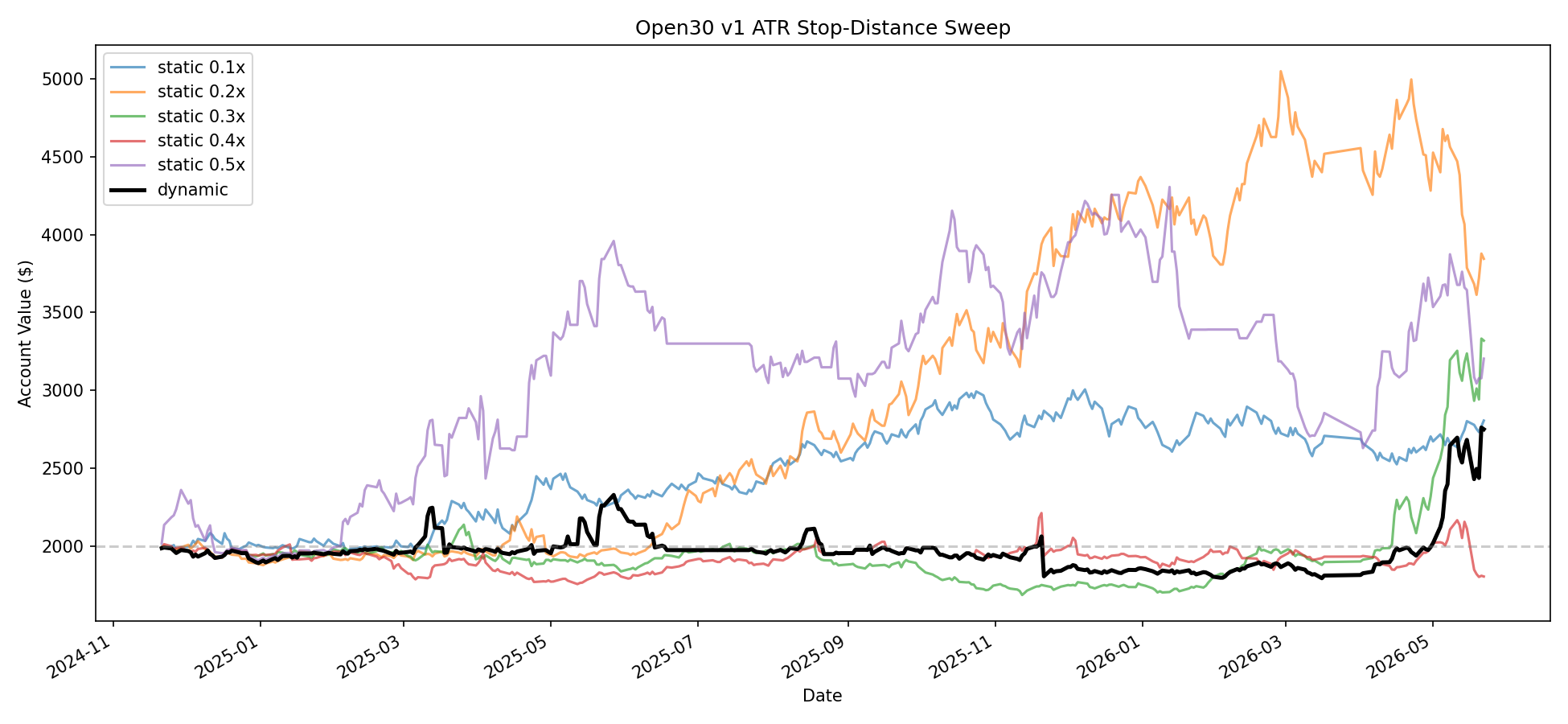

Stop-Distance Sweep

The stop-distance sweep covers a shorter recent period, from 2024-11-21 through 2026-05-22. It should be read as an experiment about stop geometry, not as a full-history replacement for the v1.x branch.

| Mode | Stop k | Trades | Mean trade return | Profit factor | Return |

|---|---|---|---|---|---|

| static | 0.1 | 364 | 10.35 bps | 1.147 | 40.23% |

| static | 0.2 | 358 | 20.72 bps | 1.193 | 92.20% |

| static | 0.3 | 358 | 15.75 bps | 1.413 | 65.91% |

| static | 0.4 | 346 | -1.84 bps | 0.935 | -9.84% |

| static | 0.5 | 287 | 23.41 bps | 1.104 | 60.12% |

| dynamic | n/a | 317 | 12.07 bps | 1.228 | 37.45% |

The recent stop sweep shows unstable stop-distance behavior: k=0.2 had the

highest account return over this window, while k=0.3 had the highest profit

factor. The dynamic selector did not dominate the static settings.

Improvement Audit

The improvement audit concluded that the long-only m=1.5 edge is real enough

to continue researching, but very sensitive to execution assumptions. The most

important tested improvements were:

- Use a fixed, cost-aware EV floor near

0.10for the long strategy. - Train a separate short-only model with a stricter EV floor near

0.25. - Deduct realistic costs and slippage from realized backtest PnL.

- Replace the fixed present-day top-25 universe with point-in-time membership.

- Explore staggered retrain consensus before heavier model families.

Reproducibility

The public export did not rerun pipelines. To reproduce results locally, either

download dataset_open30m.parquet from

mospira/open30-equity-features

and place it at data/processed/dataset_open30m.parquet, or rebuild it with

the full pipeline:

python run_pipeline.py --architecture architectures/open30_v2.yaml

python run_backtest.py --architecture architectures/open30_v2.yaml

python run_backtest.py --architecture architectures/v1_3.yaml

python run_v1_stop_distance_sweep.py

Generated outputs are written to reports/. Curated outputs in results/ are

reviewed snapshots copied from those generated reports.

Limitations

These are the main blockers before treating results as production-ready:

- Fixed present-day top-25 universe may introduce survivorship bias.

- Realized PnL does not yet fully model costs, slippage, and delayed fills.

- Labels assume the exact

09:31open. - Calibration and threshold tuning need stricter cross-fitting.

- Dynamic threshold objectives can favor low trade counts rather than daily net return.

- Retrain-calendar phase sensitivity can materially change outcomes.

- Ticker and head concentration remain meaningful.

Next Research Direction

The next high-value work is to make the simulation more execution-aware,

rebuild the universe point-in-time, and then retest the simpler m=1.5

classifier/EV design with fixed cost-aware thresholds before promoting more

complex model families.